February 09, 2026

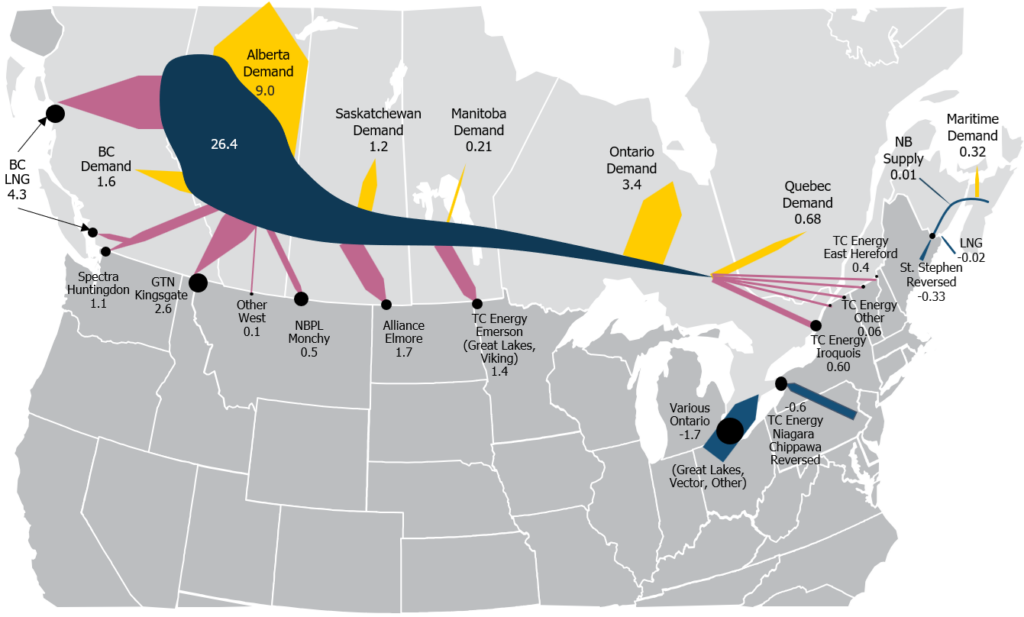

An overview of the supply-demand balance of Canadian exports/imports for 2010, 2020, 2022, 2025 and 2035 (Bcf/d).

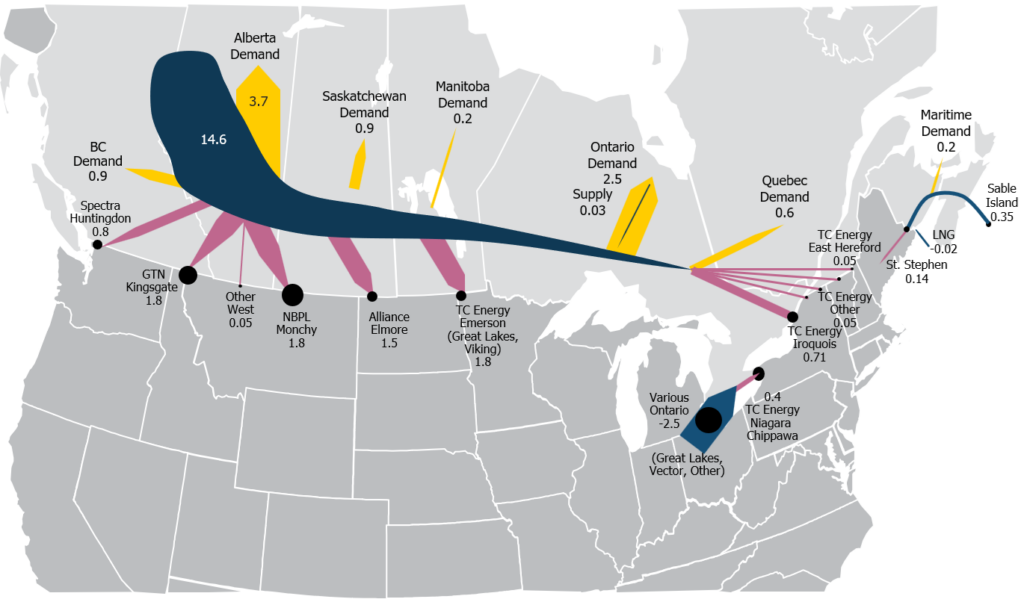

2010

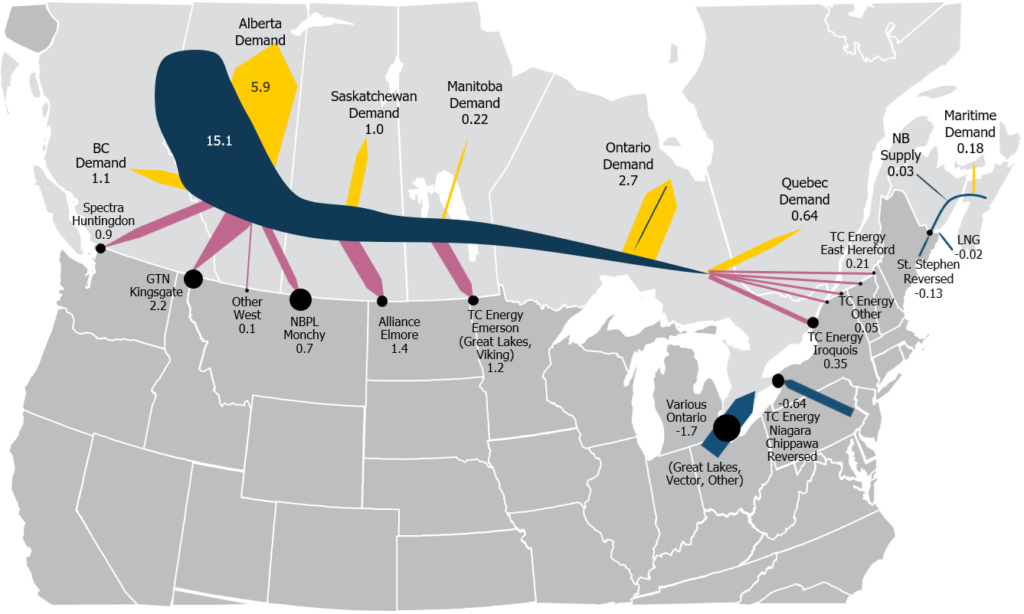

2020

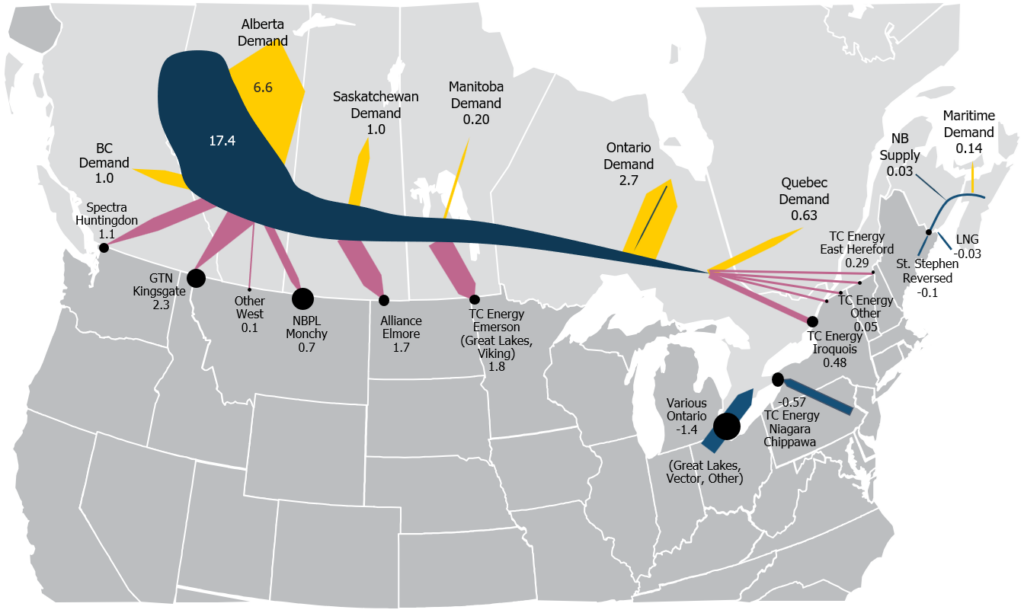

2022

2025

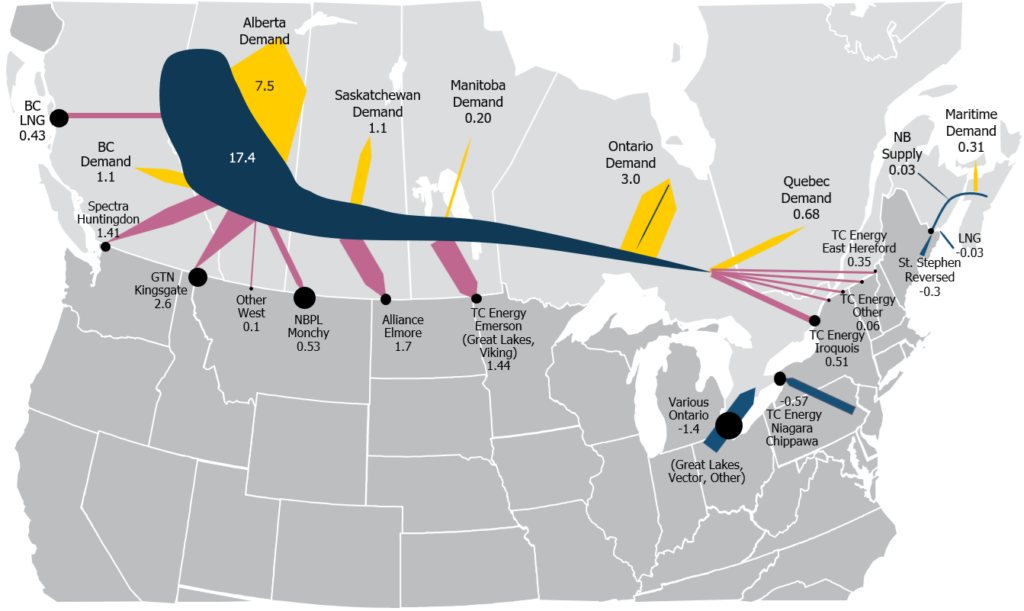

2030

2030

See Also:

Canadian Natural Gas Exports by Pipeline Forecast to 2035

Alberta and Northeast BC Natural Gas Production Allocation Forecast to 2035

Eastern Triangle Supply Sources Forecast to 2035

Eastern Triangle Exports Forecast to 2035