February 09, 2026

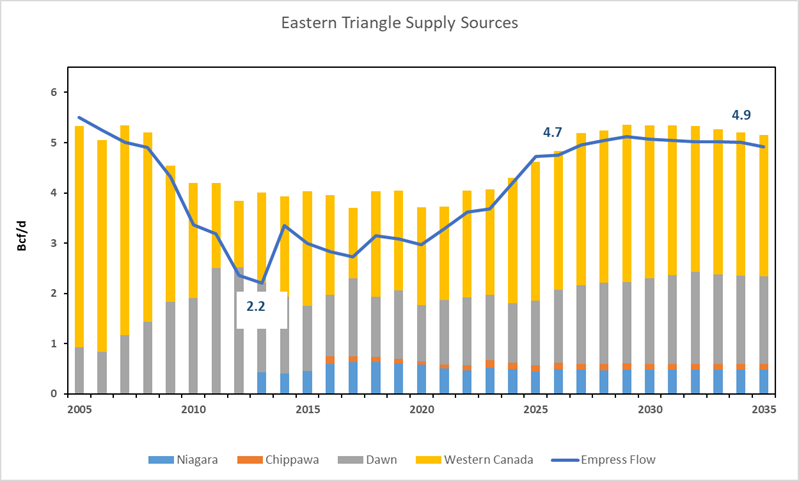

The composition of the gas supply sources to meet Eastern Triangle demand has changed over time:

- In 2005, Western Canada (TC Mainline) provided 84% of market requirements with imports at Dawn responsible for the remainder.

- By 2020, Western Canada share had decreased by almost half to 45%, with imports at Dawn (Vector now bi-directional serving Unita gas to both Chicago and Ontario) and Niagara/ Chippawa increasing in market share to 55%.

- In 2035, Incorrys expects market share of supply sources to stabilize at 50:50 with commitments to long-term pipeline capacity and increased power demand resulting from shuttered Ontario Nuclear capacity.

- Flows spurred by Dawn and North Bay LTFP commitments are expected to continue.

- Empress flows are expected to reach 4.7 Bcf/d by 2026 and 4.9 Bcf/d by 2035.

See Also:

Canadian Natural Gas Exports by Pipeline Forecast to 2035

Eastern Triangle Demand Forecast to 2035

Eastern Triangle Exports Forecast to 2035