June 11, 2026

Alberta’s Proposed Pacific Corridor Pipeline

I recently sat down with CBC’s Andrew Nichols to discuss Alberta’s push for new pipeline access to the Pacific coast. See that clip here or this one.

The interview covered a lot of ground, but there is more context worth sharing for those following this subject and Canada’s energy future.

Below is a summary of another Video I made on the same day to provide needed context, not possible in a 5-minute interview. That video is now posted on YouTube, and it can be found here.

Some Takeaways:

1. Global Oil Demand Is Rising

Global oil demand continues to grow at about 1% per year. We currently produce and consume roughly 104-105 million barrels per day. That means we need another ~1 million barrels/day of new supply annually. And we must also replace about 5.5–6 million barrels/day of annual production declines from existing fields.

Energy demand never disappears; it only increases. The same trend applies to natural gas and power, where AI-driven data centers and LNG exports are poised to increase demand. New demand is sending a signal to markets and producers, in North America, China, SE Asia and Europe.

2. Canada has the resources to help meet this demand. The question is whether we’ll build the infrastructure to get it to tidewater and new international markets.

Before 2015, Canada had four major pipeline proposals:

- Energy East (east coast tidewater) — over $1 billion spent by TC Energy before cancelling.

- Keystone XL expansion — repeatedly stalled and ultimately quashed by President Biden.

- Northern Gateway (northern Pacific) — approved by the National Energy Board but overturned by the federal Liberal cabinet; ~$600 million spent.

- Trans Mountain Expansion — the only one that succeeded, after Alberta signalled it would purchase the pipeline. Ultimately the Federal government stepped in to purchase Trans Mountain from Kinder Morgan to de-risk the project; now flowing an additional ~590,000 barrels/day.

3. Pipeline companies have since redirected capital south of the border, to the US and Mexico where there is much less regulatory risk.

The original grand bargain was this: if a pipeline company went out, had an open season, found the barrels and the commitments, signed precedent agreements with producers to backstop it, the regulatory filings would be made, and the approvals would come – in the public interest.

Now what we’re seeing is regulatory and political opposition, the Impact Assessment Act, Bill C-48, which is the tanker ban, and many other roadblocks in front of these proposals. Only one of the four oil pipeline projects, all backed by producer barrels and commitments, proceeded through the regulatory approval stage. They have spent $billions on pipeline applications with no return. So, pipeline companies have stepped back and said, “We’re out. You need to de-risk this.”

They’ll take their money and spend it on projects in the U.S. and even Mexico. Enbridge and TransCanada are busy building out their pipeline infrastructure south of the border as we speak, and investment in Canadian pipelines and in the upstream has dried up.

4. Government of Alberta documents obtained by the CBC outline three northern routes and a potential southern option, all involving complex terrain, river crossings, and traversing First Nations’ territories.

Alberta is actively consulting impacted communities and has created an investment vehicle for Indigenous ownership and participation in any new project.

All the northern routes access tidewater at Kitimat / Prince Rupert, or at various other proposed deepwater ports further north in British Columbia. The Alberta document also refers to possible Pacific access in the Vancouver area, the so-called southern route, likely along the Trans Mountain right-of-way.

5. An option also outlined in the Alberta document is possible submission to the Federal government for a pipeline corridor.

This is likely to be a designated corridor wide enough to accommodate an oil pipeline and could perhaps allow other future infrastructure along the same right of way, such as power transmission or a natural gas pipeline.

This idea would need to be fleshed out, but it has some advantages. The First Nations’ consultations could be handled up-front by both levels of government, the land could be set aside, ostensibly under federal jurisdiction utilizing s.92 constitutional powers to designate or appropriate for the general advantage of Canada.

This would effectively de-risk the pipeline route, sending a signal that there is political will. Pipeline companies (like TC Energy or Enbridge) could then secure long-term commitments from producers and move forward to flesh out a commercial project.

6. My view is that the northern routes are physically and fundamentally best.

They are a closer sail to major Asian markets (about 3 days closer). And a straight shot west (shorter) from either Fort McMurray or Edmonton, meaning hundreds of kilometres shorter, and less pipe.

Southern Port Issues:

- In Vancouver, VLCC’s (Very Large Crude Carriers) cannot load, meaning dredging or more tanker traffic (from smaller tankers).

- An egress point around Tsawwassen / Point Roberts is likely to have the same tanker access issues.

- Port Congestion: Vancouver would need to double tanker traffic in an already busy port, – the more traffic, the more chance of an accident. A northern deepwater port would be much less busy than Vancouver.

7. Is the industry standing still while an Alberta Pacific Corridor pipeline is being fleshed out?

- Trans Mountain Expansion (debottleneck) → will add ~300 Kbpd of Pacific tidewater access, this is explicitly mentioned in the MOU and is in addition to the proposed 1 MMcf/d new Pacific pipeline.

- Enbridge expansions into the U.S. → ~400 Kbpd of additional southbound capacity

- Proposed Bridger Pipeline → 550 Kbpd south to Wyoming (and ultimately U.S. Gulf Coast markets), utilizing the already approved Keystone XL route on the Canadian side.

- These add up to well over a million barrels per day, with much less risk to industry.

8. The MOU and Implementation Agreement

- The MOU includes a workaround with respect to the Bill C48 tanker ban on the northern Pacific Coast. This is positive, but why not just repeal C48?

- The MOU explicitly links the Pathways Carbon Capture and Storage (CCS) Project to the new pipeline, the so-called ‘grand bargain’.

- No Pathways. No pipeline.

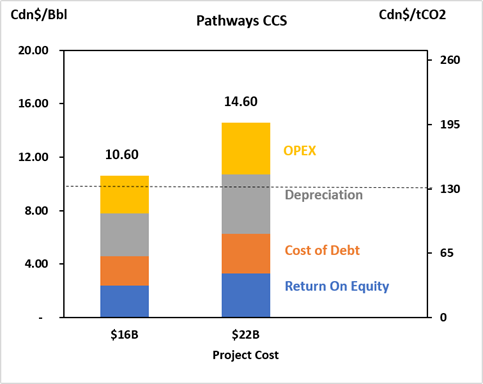

9. The Problem with Pathways CCS

Incorrys has examined the cost and economics of the Pathways Project. The latest estimate is a cost of CAD$22Billion.

When the project costs are plugged into a simple utility model, with a 40:60 equity to debt split, a nominal rate of return, estimated operating costs, depreciation, etc., the per barrel cost works out to CAD$14.60 per barrel, or just over CAD$200 per tCO2. This is significantly higher than the carbon price maximum floor of CAD$110 per tCO2 also agreed in the May 15 Implementation agreement.

Alberta and Ottawa have reportedly agreed to bear roughly 50% of the cost. Leaving producers with $7.30 per barrel. And this cost would be an expense for producers, meaning that taxpayers will be paying more than 50% of the cost.

On Pathways, and the current net-zero energy policy framework, Cenovus CEO Jon McKenzie recently stated that “…we have created a set of national policies and regulations that make resource development and investment in Canada uncompetitive with the rest of the world.” And on June 10th, at the Global Energy Show in Calgary, he told an international audience that current Canadian carbon policies make new resource investment for barrels to fill a new pipeline, “unfinanceable.”

Capital is mobile, and other less risky pipeline proposals exist, with TMX debottlenecking, Enbridge expansion and Bridger:

- Why would an Asian buyer in Korea or Japan pay a premium of some CAD$15 per barrel for oil coming off a new Pacific corridor pipeline?

- There is competition – buyers can take barrels from the US, Venezuela or new Vaca Muerta barrels from Argentina.

- And why is Canadian industry forced to bear the costs of Pathways CCS when our competitors don’t?

- CCS costs added for no benefit. So-called non-decarbonized barrels will simply fill new demand.

- Why would taxpayers pay over half the cost of Pathways, with concerning levels of government debt(s) (exacerbated by declining infrastructure investment)?

10. Timing

Alberta aims to submit its proposal by July 1, 2026, with federal approval targeted for October 2026 and construction scheduled to commence by September 2027. These are aggressive but achievable timelines — but only if there is political will.

11. Political Will

There are divisions in both the Federal and Alberta cabinets. On the Federal side, 14 Liberal MP’s recently submitted a letter expressing their disapproval of the Alberta MOU and Implementation Agreement. And former Environment Minister Steven Guilbealt has announced he will resign as a Liberal MP over the government’s environmental policies.

Meanwhile, in Alberta, the UCP cabinet is dealing with a separatist movement, broadly reflected in caucus and cabinet, and a scheduled referendum (on a referendum) on separation this coming October.

The pressure is on both PM Carney and UCP Premier Smith.

And the Pathways CCS / carbon price economics don’t work for industry.

There will never be unanimity. No matter which route is chosen. Rivers will be crossed, traditional First Nations’ territories will be traversed, mountain ranges will need to be crossed.

Jurisdictionally, Section 92 of the Constitution gives the federal government the authority to designate a pipeline, or any project, for the general advantage of Canada.

Perhaps a designated corridor along one of the proposed routes to the northern coast can be appropriated, even over the protestations of some First Nations and the Eby (BC) government. Once a corridor is set, and de-risked, then I would expect a formal pipeline could emerge quickly.

A new Pacific Corridor pipeline, developed with meaningful Indigenous partnerships and equity and strong de-risking, represents a pragmatic path forward for economic growth, energy security, and responsible resource development.

But the whole deal needs to be restructured.

— Edward Kallio

Executive Advisor, Incorrys Inc.

Calgary, Alberta

www.incorrys.com